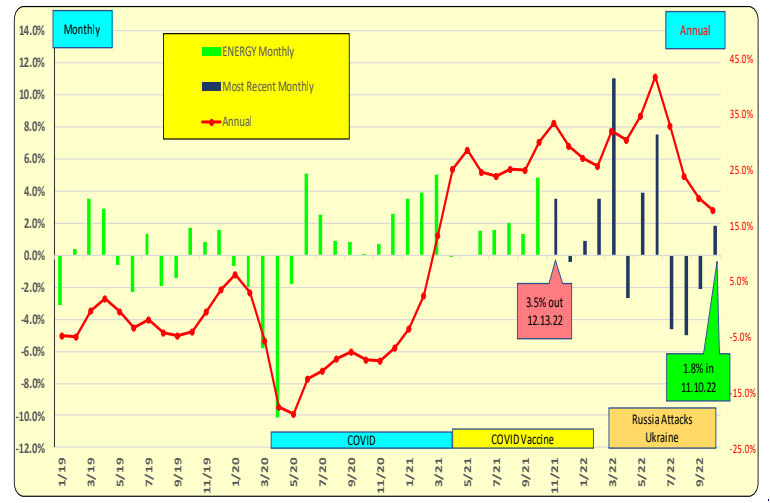

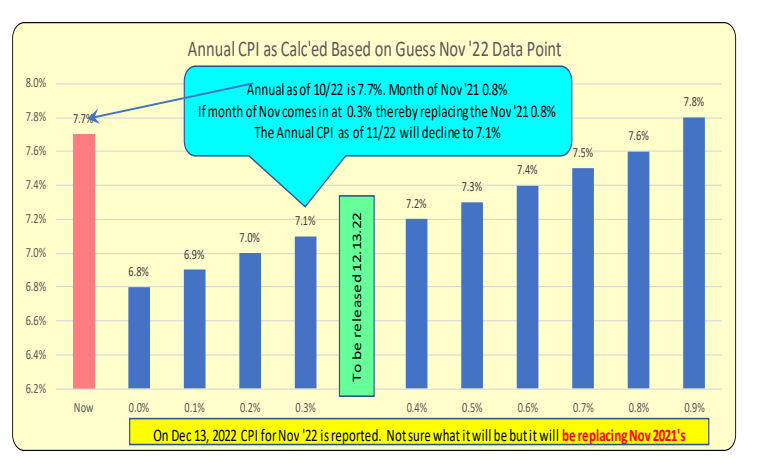

INFLATION Forecast: The annual CPI total reported each month is a combined string of 12 months of data, think of it as being 12 dominoes, a new one comes on, the oldest one drops off. THESE are the 2 dominoes to look to see if things got better or worse. If Nov ‘22 is 0.3% it will replace the Nov ‘21 data point of 0.8% on 12.13.22 and the annual CPI will decrease from 7.7% to 7.1%

Energy prices have been THE major driver of inflation in 2022. The Nov ’21 data point of 3.5% will drop off 12.13.22 and given how energy prices have been declining over the past 6 weeks, the month of Nov ‘22 should be considerably less than the Nov 21 3.5%. Housing caused inflation will also improve.

It is a hunch that November’s monthly rate will be 0.3% when the actual is announced on 12.13.22. It could be higher or lower. As such the annual CPI for November will change accordingly. Below is a range of November monthly from 0.0% to 0.9%. The resulting annual totals will range from 6.8% to 7.8%

10 Year US Treasury

On 11.10.22 the monthly CPI for Oct ‘22 came in at 0.4% and replaced the Oct ‘21 0.9%. As such the annual CPI declined from 8.2% to 7.7%. The bond market rallied and the 10 Year US Treasury declined by nearly 50bp over the four days.

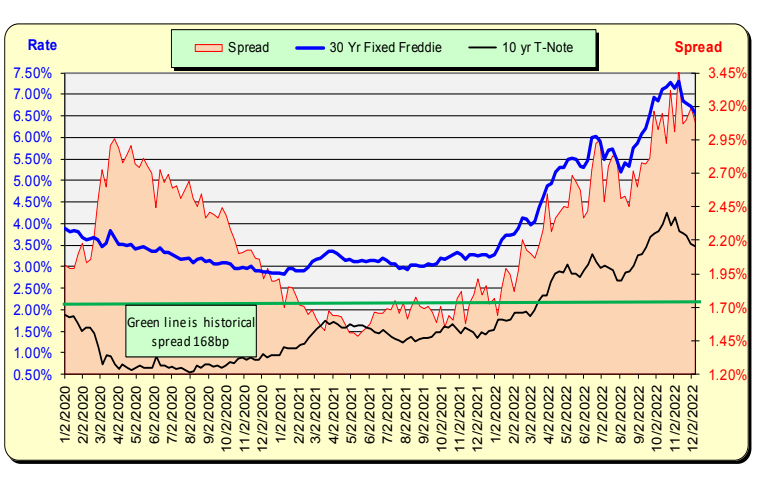

Mortgage rates are 140bp ABOVE historical average of 168bp. If mortgage pricing personnel sense that the worst of inflation is behind us and further shocks are less likely, it is foreseeable they will gradually start reducing this “cushion” premium. A 10bp to 15bp is very possible.

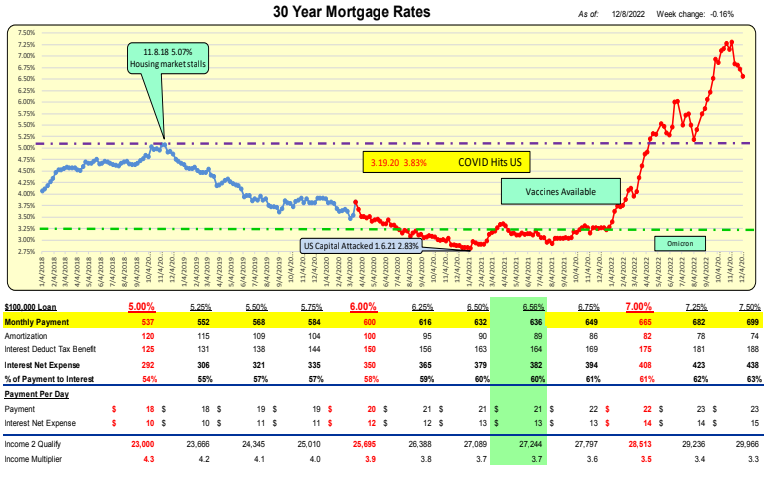

30 Year Mortgage Rates

Mortgage rates are currently 6.56%. Should the monthly CPI come in at 0.3% for November and the annual comes in around 7.1%, followed by a 35bp+ decline the 10 year, decreased spreads and the Fed raising the Fed Funds rate by a reduced 50bp on 12.14.22, it is possible we could have mortgage rates under or around 6.0% by December 30, 2022.

Bill Knudson, Research Analyst Landco ARESC