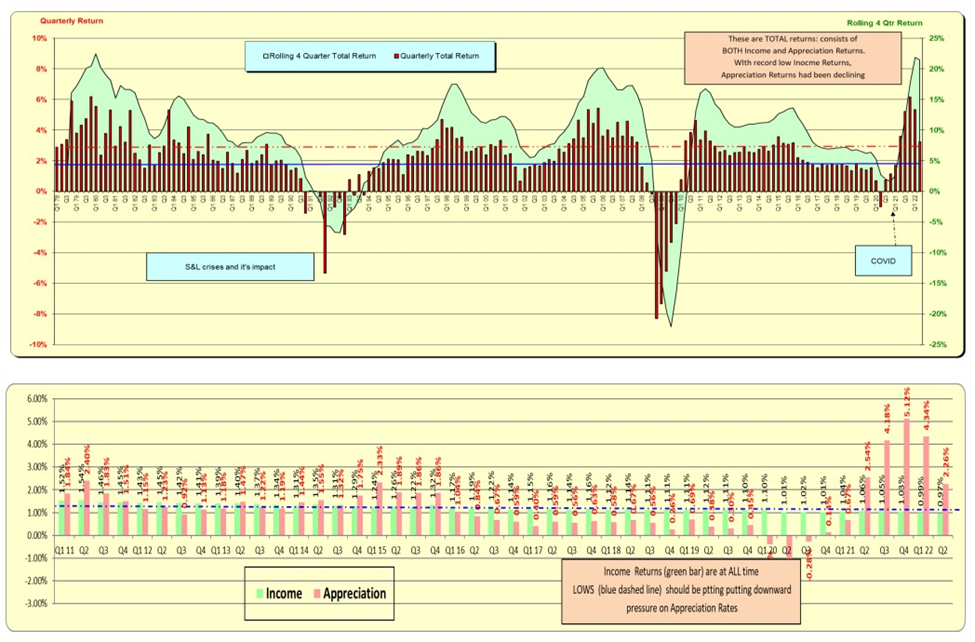

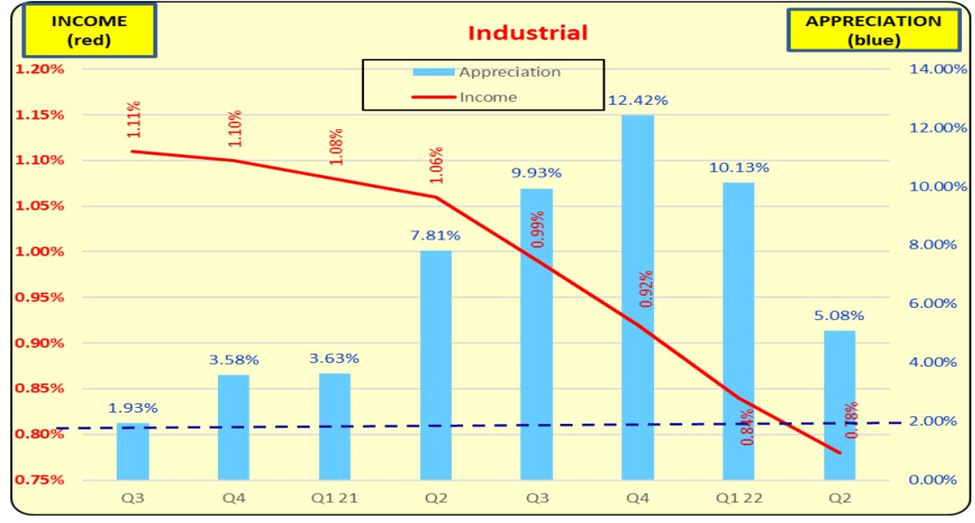

Q2 2022 returns are HALF of the prior quarter. The 4-quarter return remains at near record levels due to the elevated prior quarterly returns. Rising 10 Year US Treasury Rates are likely a factor. Industrial properties had the lowest Income Return but had the highest appreciation Return which is near RECORD levels. Industrial income return is at its LOWEST LEVEL EVER. Annual return for Q4 came in at a near record rate of 21.89% driven primarily by Industrial properties. Note in the lower graphic that quarterly income returns are DECLINING.

Total Returns – Income and Appreciation Returns

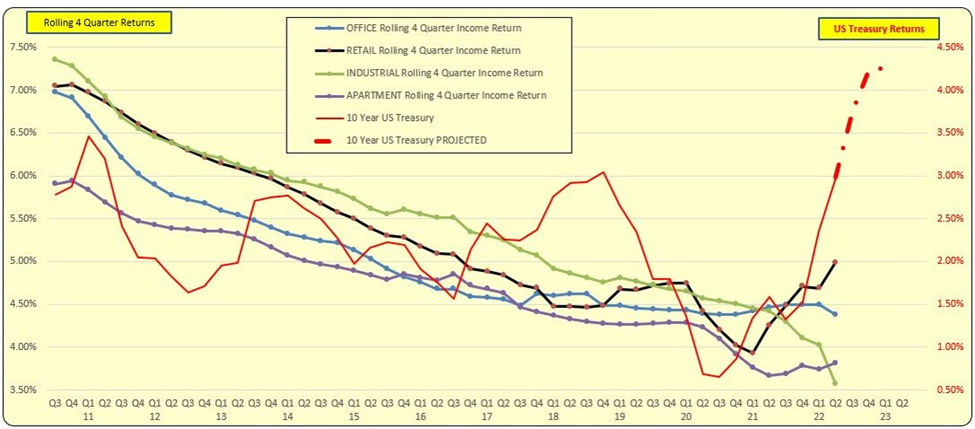

The main driver of the ANNUAL return was industrial property returns of 48%. In NCREIF’s ~47-year history, this is near the highest ANNUAL return for ANY PROPERTY TYPE. Apartments were next with 24% followed by Office and Retail with ~7%. It was noted that BOTH NCRIEF INCOME Returns and the US 10 Year Treasury rates were at or near RECORD LOWS in 2021. It was also noted that the 10 Year Treasury rate had decreased during most of this time of 2011-2021.

On 3.16.22 the Federal Reserve clearly stated that interest rates will be increased. The red dashed line is the projected 10 Year Treasury rate through the end of 2022 in the below graph. While there may not be a direct cause and effect relationship between the 10 Year Treasury and NCREIF Income and hence Appreciation returns, there is a correlation This correlation is material over longer time periods and will likely have an adverse impact on future property valuations and returns. US 10-Year Treasury Rate and Rolling 4 Quarter Income Returns have a high correlation. Property returns in essence are risk-based relative to the US Treasury 10-year rates—which dramatically increased in Q1 and Q2. The dashed red line is projected rates thru yearend based on the Fed’s 3.16.22 “dot plot” of anticipated rate increases thru 2022. This would have a material impact on both income and appreciation returns going forward.

Projected 10 Year Treasury Rate

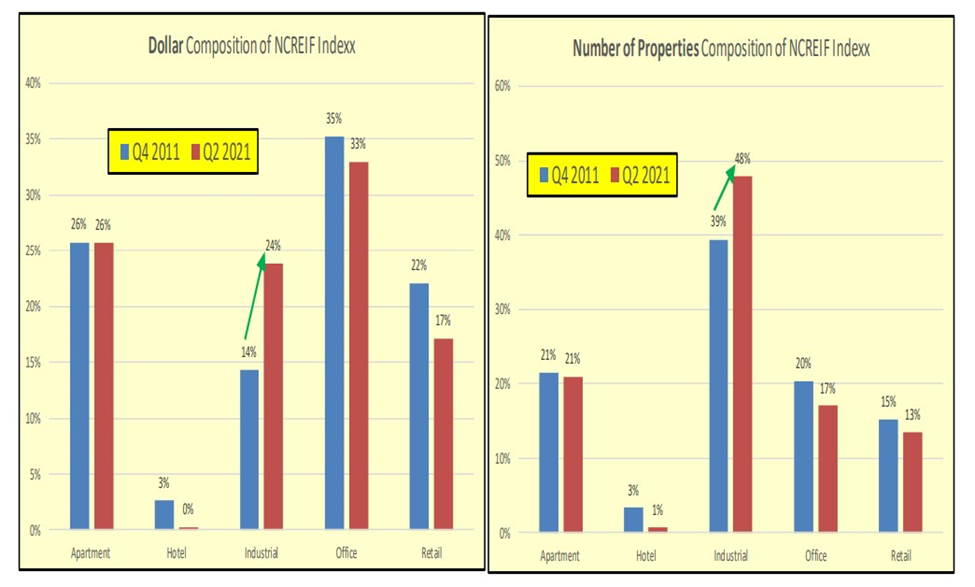

INDUSTRIAL PROPERTIES as a % of NCREIF: NCREIF’s composition by property type gradually changes over time. Below is the changes from the 10-year period from Q4 2011 to Q2 2021. There has been a material increase in Industrial Properties. Because of this composition change, the Total NCREIF return is higher due to record-shattering returns posted by industrial properties.

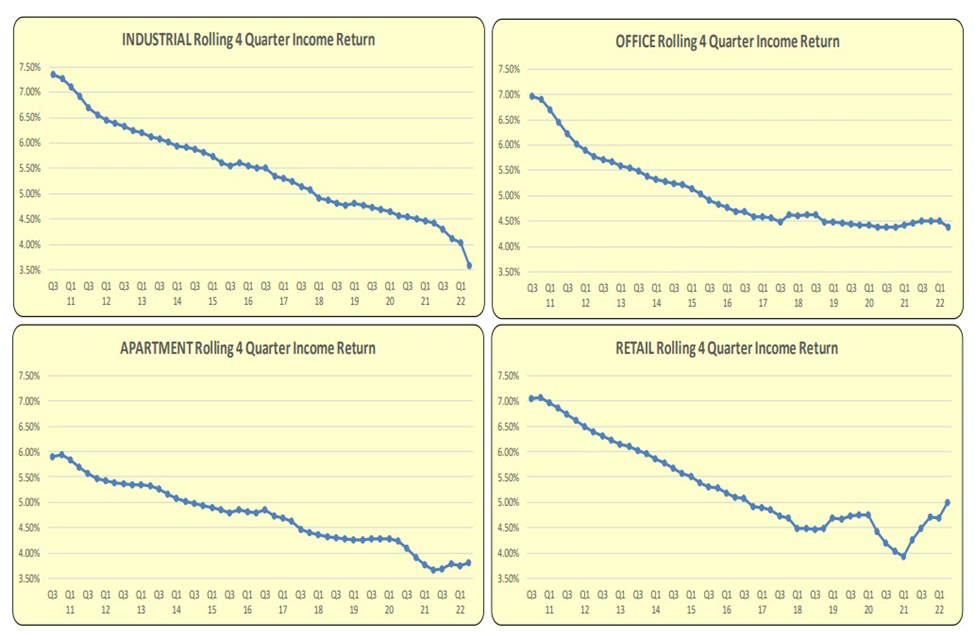

Industrial properties had the lowest Income Return but had the highest appreciation Return which is near RECORD levels. Industrial income return is at its LOWEST LEVEL EVER.

Rolling 4 Quarter Income Returns for all 4 property types are near record lows. This implies cap rates are also near record lows. Note Industrial’s decline in the most recent quarter.

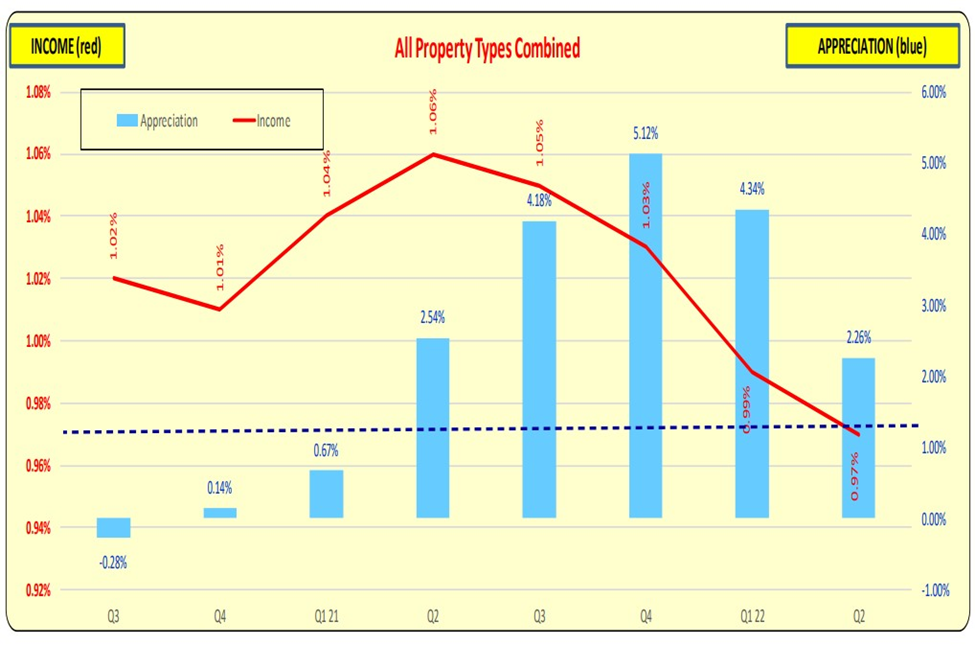

Income returns are tapering off as appreciation increases are recorded. The appreciation returns materially declined in Q2.

ALL PROPERTY TYPES COMBINED

Total returns are being driven by record-shattering Appreciation returns. Income returns have been decreasing indicating that FUTURE income increases are anticipated, or CAP RATES are decreasing. With rising 10 Year Treasury rates, whether the lower cap rates can be maintained is subject to debate. It is true that demand for Industrial property increased during the 2020-2022 COVID outbreak as people stayed home and did more online shopping. With COVID becoming less of a public policy issue, it remains to be seen if the online shopping trend will remain at high levels.

INDUSTRIAL

Income returns increased slightly in Q2, and the appreciation return was negative.

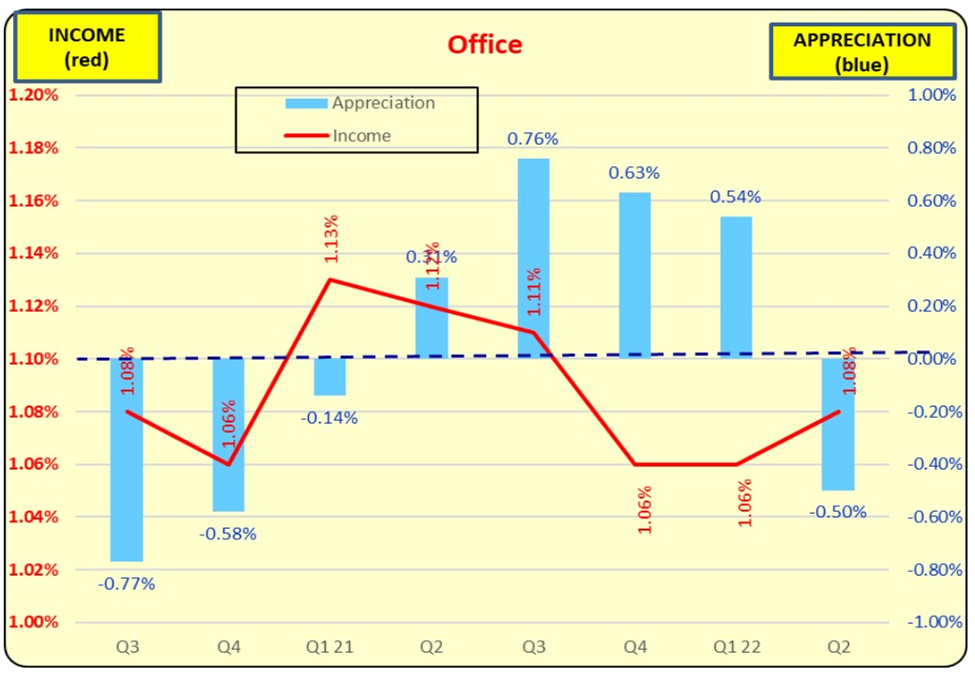

OFFICE

Income returns have been relatively flat. Appreciation plummeted in Q2 2020 COVID but has improved since then.

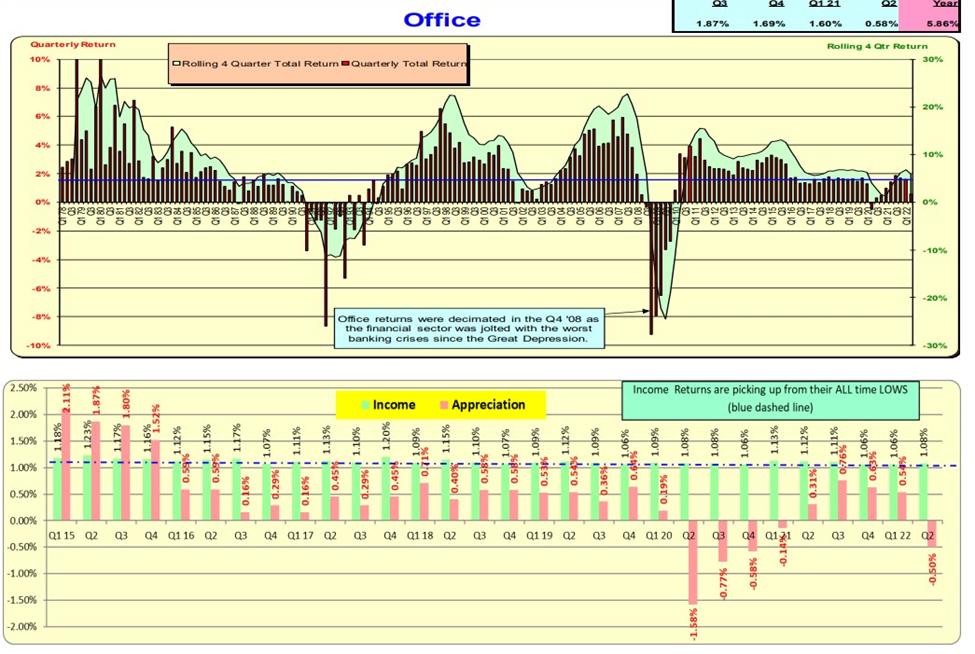

OFFICE

Income returns bottom out in Q4 2020 when record-low mortgage occurred and have risen since Q4 2021. Appreciation returns have followed a similar pattern.

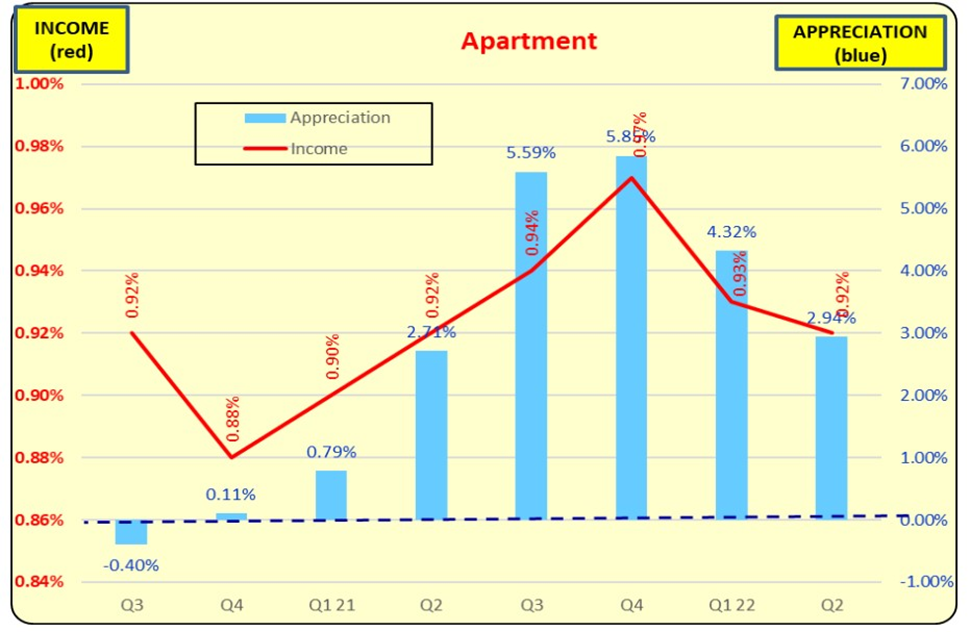

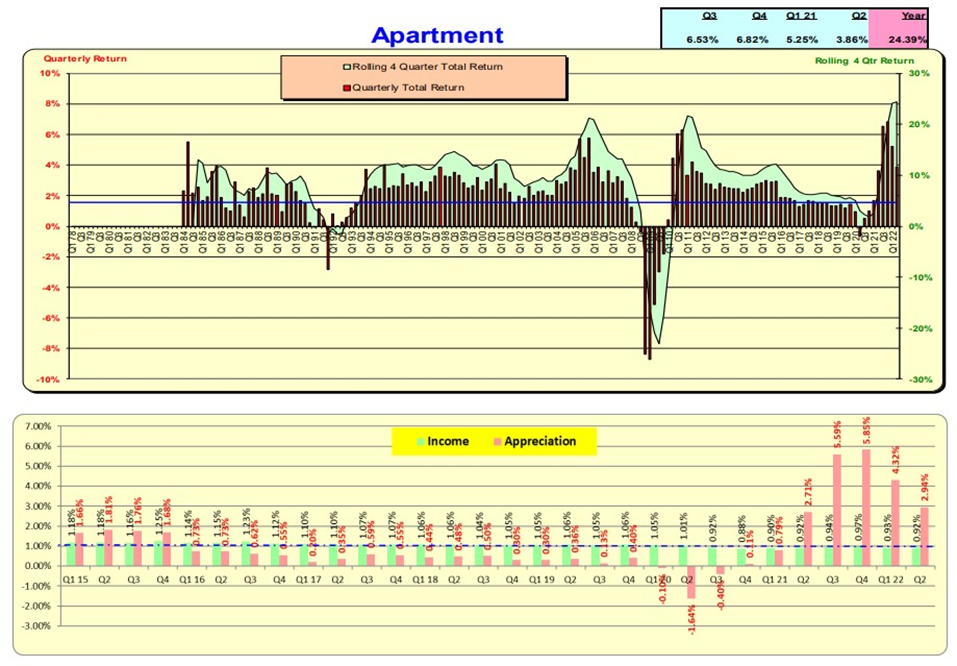

APPARTMENT

INCOME returns increased driving APPRECIATION RETURNS to record highs.

APPARTMENT

Income returns have been slowly increasing as property appreciation has modestly increased.

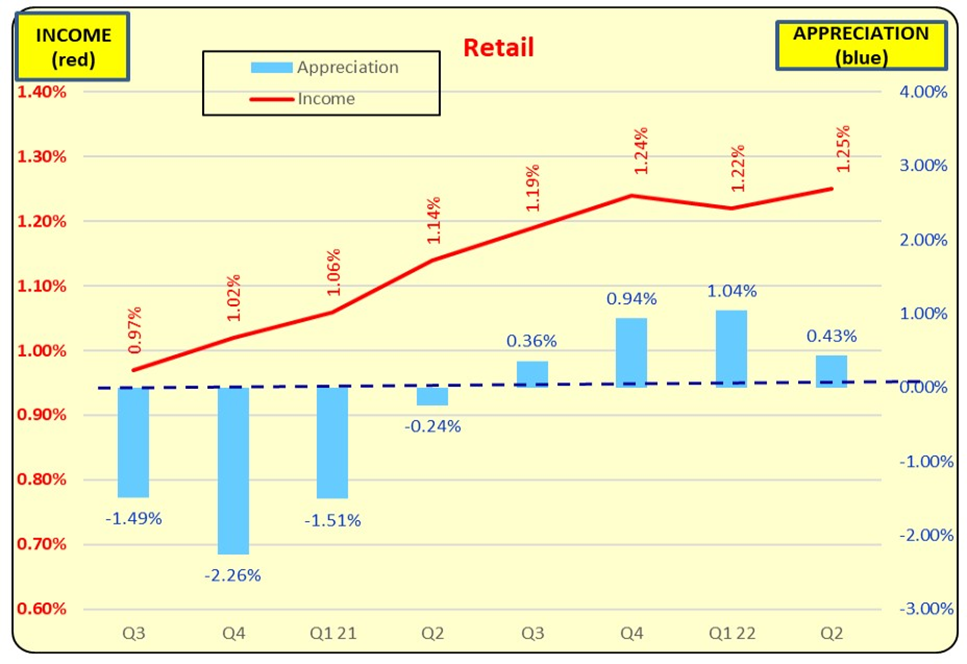

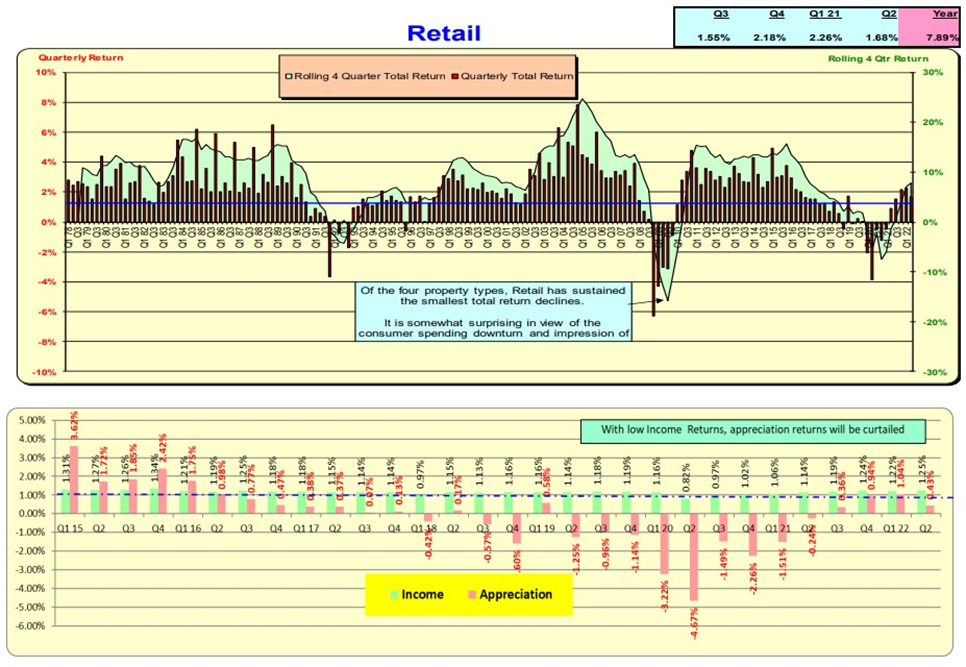

RETAIL

As INCOME returns have slowly increased, appreciation returns have also modestly increased. Q3 Q4 Q1 21 Q2.

RETAIL

Bill Knudson, Research Analyst Landco ARESC