The answer is YES.

While many, including myself, have focused on Treasury rates rocketing up, no one has mentioned how STEEP short-term rates are. The Fed has done only movement from 0.25% to 0.50%. The Fed controls short-term rates while long-term rates are determined by the market, and the market has priced in the number of future Fed Fund rate increases hence the STEEP short-term rate portion of the yield curve.

With the STEEP short-term portion of the Yield Curve, the Fed can increase Fed Funds by nearly 200 bps and yet have no changes in longer-term Treasuries (ie 5+ years). The result can still have a “normal” shaped Yield Curve. In fact, a Yield Curve shape is very similar to the pre-COVID-19 Yield Curve.

What is of note, let’s assume no change in 5+ rates, the spread of Mortgage to 10 Year is ~70bp above historic spread. If half of this “spread premium” decreased, we’d be looking at mortgage rates of under 5.00% again.

5.00% is an important price point for Millennials. In my opinion, they will slow house purchase decisions when rates are above 5.00%. Hate to say it, but the Millennials are the Power Consumers of America now since the Baby Boomers have aged out of this consumption function.

Timeline of Yield Curve

BEFORE, DURING, and AFTER COVID-19. Before COVID-19 is the green line—note how relatively flat it is. No indication that COVID was about to hit. The blue line is AFTER COVID-19 when the Fed reduced Fed Fund rates by 150bp in 2 weeks and started their QE program called Taper which brought down long-term rates. By the end of 202/beginning of 2021 vaccines were being rolled out. By the end of 2021/beginning of 2022 vaccines and boosters were widely administered and the economy’s recovery was moving forward (dashed line). Long-term rates returned to PRE-COVID-19 LEVELS. With the recovery underway, inflation pressures occurred, and short rates started to increase with anticipation of the Fed increasing rates. (red line).

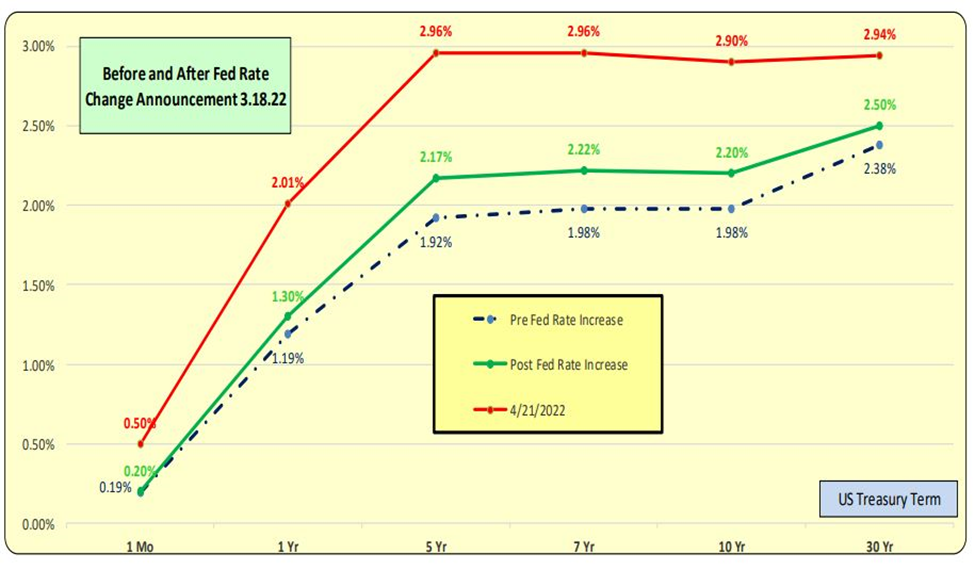

Fed Announces Material Rate Increases

In March 2022 the Fed announced that material rate increases were on the horizon (dashed is before, the green line is after). While the yield curve is flat for 5+ year terms, what is seldom mentioned is how STEEP short-term rates are. Long-term rates are substantially ABOVE PRE COVID-19 levels. The Fed controls short rates while the market determines longer-term rates, and it appears the market has already priced in substantial future rate increases by the Fed.

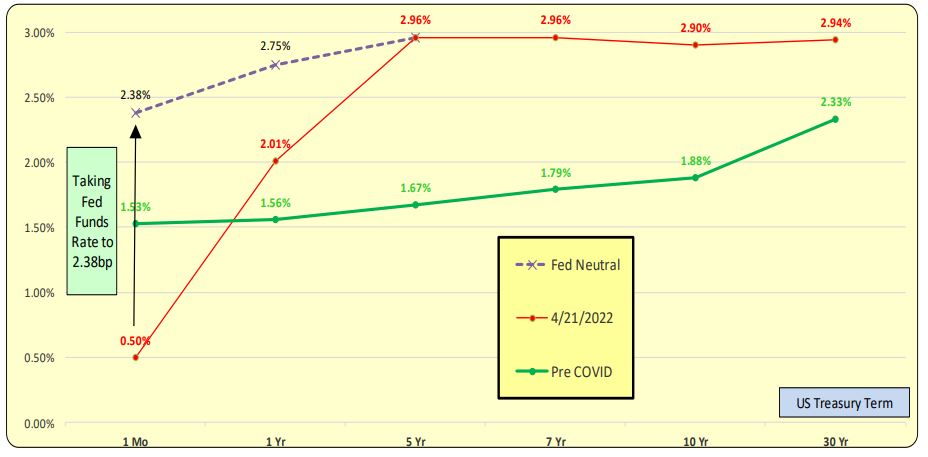

Fed’s Indicate Increasing Fund Rates

Some Fed members have indicated increasing Fed Fund rates from their current level of 0.50% to 2.38%. The red line is the April 21st, 2022 yield curve. Note how STEEP short-term rates are. With Fed Funds at 2.38%, the result is the dotted line AND with NO changes to 5+ term rates. The resulting yield curve would be the combined dash line and red line for 5+. The shape of this yield curve is very similar to the PRE COVID yield curve but at higher rates. With mortgage rates being 70bp above the long-term spread of mortgage to 10 years, mortgage rates could decrease; taking just half of it will be <5.00% mortgage rates The result is a Fed Funds rate level that is neutral to the economy: does NOT expand or constrict.

Bill Knudson, Research Analyst Landco ARESC

One Response

Thank you for your inquiry. Weekly there are reports on US treasury and mortgages. CPI is monthly and quarterly there are reports on economic indicators. Periodically, we will offer a piece on overall performances of the real estate market, and by different sector.